The Big Beautiful Bill and What It Means for Your Wallet

The “Big Beautiful Bill” (BBB) represents one of the most sweeping federal tax reforms since the 2017 Tax Cuts and Jobs Act (TCJA). It includes income tax cuts, new savings vehicles, expanded deductions and credits, as well as targeted provisions for working parents, seniors, and small business owners. Simultaneously, it rolls back many clean energy tax breaks and tightens eligibility standards for certain federal benefits, signaling a strategic pivot in fiscal priorities.

Whether you are a hard-working professional, a retiree, a small business owner, or someone planning for your children’s future, the BBB likely contains provisions that will affect your financial plans.

Below, we break down the most important sections and what they mean for your money in practical terms.

1. Income Tax Rate Cuts

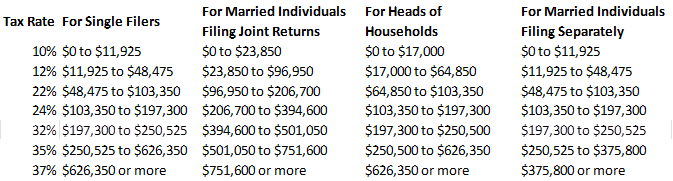

The BBB locks in the reduced marginal tax rates from the TCJA, maintaining the current lower tax brackets for individuals and families. It also preserves inflation indexing.

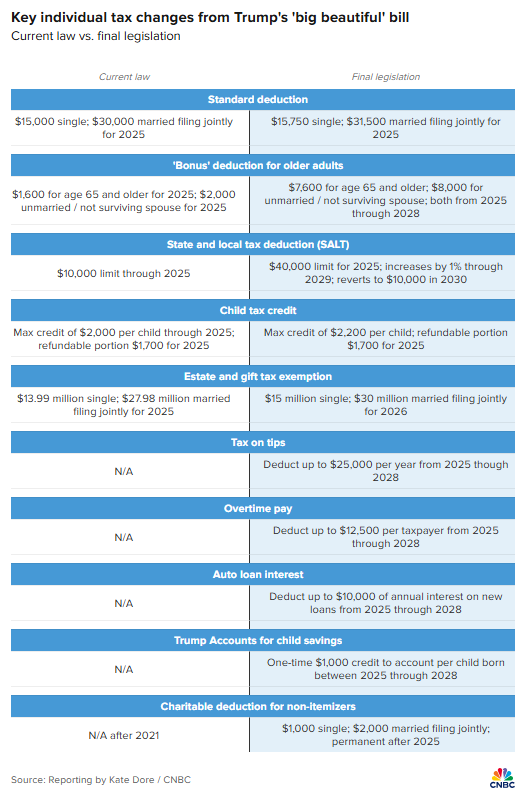

2. Standard Deduction

The 2025 standard deduction is getting a small boost:

- Single: from ~$15,000 → $15,750

- Married joint: from ~$30,000 → $31,500

New $6,000 deduction for seniors – available to individuals with up to $75,000 in modified adjusted gross income and $150,000 if married and filing jointly. The temporary senior deduction would be in place for tax years 2025 through 2028.

3. Child Tax Credit (CTC)

The Child Tax Credit increases to $2,200 per child and is now indexed to inflation. Both parents and children must have Social Security Numbers to qualify.

4. Qualified Business Income (QBI) Deduction – Section 199A

The Big, Beautiful Bill introduces several significant changes to the Qualified Business Income (QBI) deduction under Section 199A. These updates make the deduction more generous, permanent, and easier to navigate for pass-through business owners.

- Permanent Extension: The QBI deduction, previously set to expire after 2025, has been made permanent. The Bill ensures that eligible pass-through entities, including sole proprietorships, partnerships, and S corporations, continue to receive tax benefits.

- Increased Deduction Rate: The deduction rate rises from 20% to 23% of QBI, qualified REIT dividends, and income from publicly traded partnerships (PTPs), increasing overall tax savings.

- New Limitation Rules for High-Income Taxpayers: For those with taxable income above $394,600 (joint filers) or $197,300 (others) in 2025, the current phase-in rules are replaced by a two-step calculation

- Step 1: The deduction (23% of QBI) is limited to the greater of:•: 50% of W-2 wages, or• 25% of W-2 wages + 2.5% of the unadjusted basis (UBIA) of qualified property. Specified Service Trades or Businesses (SSTBs) receive no deduction in this step.

- Step 2: Calculates 23% of QBI from all businesses (including SSTBs), without wage limits. This amount is reduced by 75% of the excess taxable income above the threshold.

- The final deduction is the greater of the Step 1 or Step 2 result.

- Inflation Indexing: Starting in 2026, income thresholds will be adjusted annually for inflation, allowing more taxpayers to qualify over time.

- Expanded Eligible Income: Qualified Business Development Company (BDC) interest dividends are now included alongside REIT dividends and PTP income.

- Broader Phaseout Ranges for SSTBs: The income phaseout range for SSTBs increases from $100,000 to $150,000 (joint filers) and from $50,000 to $75,000 (single filers), allowing more high-income SSTB owners to claim the deduction.

- Minimum Deduction: Beginning in 2026, taxpayers with at least $1,000 in business income will receive a minimum QBI deduction of $400, even if they otherwise wouldn’t qualify.

5. Estate and Gift Tax

The Bill raises the Estate and Gift Tax Exemption to $15 million for single taxpayers and $30 million for married filing jointly for 2026

6. Alternative Minimum Tax (AMT)

The BBB makes the higher AMT exemptions from TCJA permanent. However, it reverts the AMT income phaseout threshold to $500,000 for single filers and $1 million for joint filers. The phaseout rate also increases from 25% to 50%, accelerating reductions for high-income taxpayers starting in 2026. The changes will primarily impact high-income earners. Tech workers who exercise ISOs may also be subject to a higher AMT.

7. Mortgage Interest & Casualty Losses

The BBB restores the deduction for mortgage insurance premiums and continues to limit casualty loss deductions to those resulting from federally declared disasters. The limit on mortgage interest deduction remains at a $750,000 loan balance.

8. SALT Deduction Cap (State and Local Taxes)

The BBB significantly expands the State and Local Tax (SALT) deductions. The cap increases to $40,000 in 2025 but phases down rapidly for higher-income earners and is scheduled to sunset in 2029, reverting to $10,000.

- The cap is raised to $40,000 starting in 2025.

- The phaseout begins at a MAGI of $ 500,000 and phases down to $10,000 by a MAGI of $600,000.

- Indexed for inflation through 2029.

- Sunsets in 2029, reverting to a $10,000 cap permanently thereafter.

9. No Tax on Tips

The Big Beautiful Bill introduces no tax on tips.

- Tip income up to $25,000 per year is excluded from gross income.

- It applies to cash and non-cash tips (e.g., credit card tips and digital payments).

- Phaseout thresholds:

- It begins at $150,000 for single filers.

- It starts at $300,000 for married filing jointly.

- Above these thresholds, the exclusion phases out proportionally and is eliminated beyond the top income limits.

- Employers must still report total tip income on Form W-2; however, the IRS will allow for partial or full exclusion based on the taxpayer’s income and the amount of reported tips.

10. No Tax on Overtime Pay

The Bill also introduces no tax on tips.

- Excludes up to $12,500 per year in overtime wages from federal income tax or $25,000 for married filing jointly.

- Applies only to hours worked beyond 40/week as defined by FLSA (Fair Labor Standards Act).

- The tax break begins to phase out once earnings exceed $150,000 and $300,000 for joint filers. Any overtime pay exceeding $12,500 is taxed at the standard federal income tax rate.

- Aims to incentivize extra work without pushing employees into higher tax brackets.

11. No Tax on Car Loan Interest

- Deducts interest paid on personal auto loans (primary vehicle only).

- Capped at one vehicle per taxpayer, and interest is limited to $10,000 per year.

- Available to non-itemizers as an above-the-line deduction.

- Subject to AGI threshold of $100,000 for single filers and $200,000 for joint filers

- The tax break applies to car purchases made from 2025 through 2028.

- The vehicle must be assembled in the United States to qualify.

12. “Trump Accounts” and Contribution Pilot Program

The Big Beautiful Bill introduces a new savings account for children. I like the idea that each newborn child will receive $1,000 matching contribution from the government.

- Creates a new class of tax-advantaged savings accounts (“Trump Accounts”).

- Includes a pilot federal matching program for contributions up to $1,000/year for qualified children born in 2025 through 2028.

- All contributions will be made with pre-tax dollars with a $5,000 annual limit,

- Earnings grow tax-deferred, and qualified withdrawals are taxed as long-term capital gains.

- Account owners can use qualified rollover contributions to fund Trump accounts.

- Employers may contribute up to $2,500 per year to employees or their dependents on a tax-free basis.

13. Childcare & Dependent Care Credits

The dependent care FSA cap increases from $5,000 to $7,500, providing more relief to working families who juggle childcare and eldercare costs.

14. Adoption Credit

The adoption credit increases to $5,000 per child. It is now more inclusive of tribal and special-needs adoptions. Unused credits can be carried forward for up to five years.

15. Student Loan Benefits and 529 Plans

- Employer-paid student loan benefits (up to $5,250 per year) are permanently excluded from taxable income.

- Lifetime borrowing limit of $257,500 for federal student loans;

- Borrowing for professional degrees capped at $50,000 per year and $200,000 lifetime; for graduate students, unsubsidized loans capped at $20,500 per year and $100,000 lifetime

- Eliminates grad PLUS loans, which allowed grad students to borrow up to their entire cost of attendance minus any federal aid.

- Expands 529 plan eligibility to:

- Cover postsecondary credentialing, exams, and certification prep.

- Include payments on qualified student loans.

16. Charitable Deductions

Even non-itemizers can now deduct donations—up to $1,000 (single) or $2,000 (married).

Individuals can receive a tax credit for donations made to qualifying nonprofits that award scholarships for K-12 students to attend private schools. School voucher fund donors can claim a 100% credit on those donations, up to $1,700. The break will be available starting in 2027.

17. Remittance Transfer Tax

The BBB imposes a 1% excise tax on international wire transfers. It applies to individuals sending money outside the US.

18. Repeal of Clean Energy Credits

The Big Beautiful Bill Terminates a wide range of green energy tax credits, including:

- EV tax credit

- Home energy efficiency improvements

- Solar and wind investment credits

- Clean hydrogen and advanced manufacturing credits

- Only limited exceptions remain (e.g., nuclear).

19. ABLE Account Enhancements

The BBB includes several changes and enhancements to Achieving a Better Life Experience (ABLE) accounts, which offer savings opportunities for individuals with disabilities. Here are the key provisions related to ABLE accounts:

- Increases contribution limits of $18,000 for 2025 to ABLE accounts if they earn income and meet specific eligibility requirements

- Expands the saver’s credit for contributions to ABLE accounts. The maximum credit amount has been increased from $2,000 to $2,100, effective December 31, 2026

- Allows rollovers from 529 plans into ABLE accounts.

- Provides more flexible savings for individuals with disabilities.

20. Health Insurance Changes

The BBB imposes stricter eligibility requirements for participation in Medicaid and SNAP.

- Tightens eligibility for ACA premium tax credits. Must verify legal presence and Medicaid eligibility.

- Mandates an 80-hour-a-month Medicaid work requirement for able-bodied adults and adults with children 15 and older

- Repeals limits on recapture of advance credits (you must repay full overpayments).

- Allows bronze/catastrophic plans to qualify for Health Savings Accounts (HSAs).

- Enhances options for telehealth and direct primary care arrangements.

21. QSBS

The Big Beautiful Bill makes sweeping changes to the Qualified Small Business Stock exemption for startups and entrepreneurs. Previously, 100% exclusion required a 5-year holding period, with no partial benefits at earlier milestones.

- Increases to $15 million (up from $10 million), the gain from the stock acquisition date could be excluded from capital gain taxes.

- Reduces the required holding period for QSBS benefits for stock acquired after the applicable date from 5 years to 3 years

- Less than 3 years – 0% exemption

- 3 years holding period – 50% exemption

- 4 years holding period – 75% exemption

- 5 years or longer holding period – 100% exemption

- Retains the 10x basis rule so that the exclusion will apply to the greater of $15 million or 10x the taxpayer’s basis.

- The permitted gross assets limit increases from $50 million to $75 million.

Final Words

The Big Beautiful Bill introduces a wide range of tax and policy changes that could have significant financial implications for individuals, families, and businesses.

Many of the provisions aim to improve affordability for everyday expenses, such as childcare, education, and healthcare, while others adjust rules surrounding savings, investments, and business income. At the same time, some existing programs and tax credits—particularly in the clean energy space—are being phased out or significantly reduced, which may affect planning in those areas.

Because many changes include income thresholds, phaseouts, or sunset provisions, their effects will vary depending on individual circumstances. Some benefits are immediate, while others take effect in future tax years or build over time.

As with any comprehensive tax legislation, it’s crucial to understand how the details apply to your specific situation. Reviewing these changes carefully—ideally with guidance from a tax or financial advisor—can help ensure that you make informed decisions and take full advantage of any new opportunities available under the law.

Contact Us