A beginner’s guide to retirement planning

Many professionals feel overwhelmed by the prospect of managing their finances. Often, this results in avoidance and procrastination– it is easy to prioritize career or family obligations over money management. Doing so puts off decision making until retirement looms. While it is never too late to start saving for retirement, the earlier you start, the more time your retirement assets have to grow. There are several things you can do to start maximizing your retirement benefits. In this posting, I will present my beginner’s guide to retirement planning.

Start Early

It is critical to start saving early for retirement. An early start will lay the foundation for healthy savings growth.

With 7% average annual stock return, $100,000 invested today can turn into almost $1.5m in 40 years. The power of compounding allows your investments to grow over time.

The table below shows you how the initial saving of $100,000 increases over 40 years:

| Year 0 | 100,000 |

| Year 10 | 196,715 |

| Year 20 | 386,968 |

| Year 30 | 761,226 |

| Year 40 | 1,497,446 |

Not all of us have $100k to put away now. However, every little bit counts. Building a disciplined long-term approach towards saving and investing is the first and most essential requirement for stable retirement.

Know your tax rate

Knowing your tax bracket is crucial to setting your financial goals. Your tax rate is based on your gross annual income subtracted by allowable deductions (ex: primary residence mortgage deductions, charitable donations, and more).

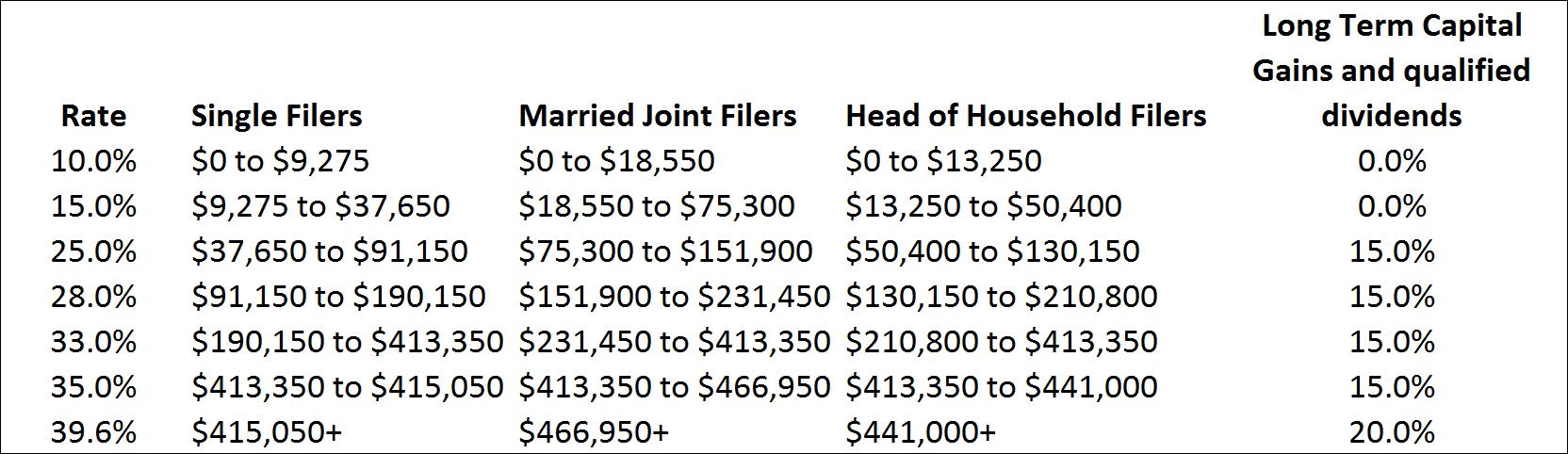

See below table for 2016 tax brackets.

Jumping from a lower to a higher tax bracket while certainly helpful for your budget will increase your tax liabilities to IRS.

Why is important? Understanding your tax bracket will help you optimize your savings for retirement.

Knowing your tax bracket will help you make better financial decisions in the future. Income tax brackets impact many aspects of retirement planning including choice of an investment plan, asset allocation mix, risk tolerance, tax level on capital gains and dividends.

As you can see in the above table, taxpayers in the 10% and 15% bracket (individuals making up to 37,650k and married couples filing jointly making up to $75,300) are exempt from paying taxes on long-term capital gains and qualified dividends.

Example: You are single. Your total income is $35,000 per year. You sold a stock that generated $4,000 long-term capital gain. You don’t owe taxes for the first $2,650 of your gain and only pay 15% of the remaining balance of $1,350 or $202.5

Conversely, taxpayers in the 39.6% tax bracket will pay 20% on their long-term capital gains and qualified dividends. A long-term capital gain or qualified dividend of $4,000 will create $800 tax liability to IRS.

Tax bracket becomes even more important when it comes to short-term capital gains. If you buy and sell securities within the same year, you will owe taxes at your ordinary income tax rate according to the chart above.

Example: You make $100,000 a year. You just sold company shares and made a short-term capital gain of $2,000. In this case, your tax bracket is 28%, and you will owe $560 to IRS. On the other hand, if you waited a little longer and sold your shares after one year you will pay only $300 to IRS.

Know your State and City Income Tax

If you live in the following nine states, you are exempt from paying state income tax: Alaska, Florida, Nevada, South Dakota, Texas, Washington, Wyoming, New Hampshire and Tennessee.

For those living in other states, the state income tax rates vary by state and income level. I’ve listed state income tax rates for California and New York for comparison.

California income tax rates for 2016:

1% on the first $7,850 of taxable income.

2% on taxable income between $7,851 and $18,610.

4% on taxable income between $18,611 and $29,372.

6% on taxable income between $29,373 and $40,773.

8% on taxable income between $40,774 and $51,530.

9.3% on taxable income between $51,531 and $263,222.

10.3% on taxable income between $263,223 and 315,866.

11.3% on taxable income between $315,867 and $526,443.

12.3% on taxable income of $526,444 and above.

New York State tax rates for 2016:

4% on the first $8,400 of taxable income.

4.5% on taxable income between $8,401 and $11,600.

5.25% on taxable income between $11,601 and $13,750.

5.9% on taxable income between $13,751 and $21,150.

6.45% on taxable income between $21,151 and $79,600.

6.65% on taxable income between $79,601 and $212,500.

6.85% on taxable income between $212,501 and $1,062,650.

8.82% on taxable income of more than $1,062,651.

City Tax

Although New York state income tax rates are lower than California, those who live in NYC will pay an additional city tax. As of this writing, the cities that maintain city taxes include New York City, Baltimore, Detroit, Kansas City, St. Louis, Portland, OR, Columbus, Cincinnati, and Cleveland. If you live in one of these cities, your paycheck will be lower as a result of this added tax. The city tax rate varies from 1% and 3.65%.

Create an emergency fund

I recommend setting up an emergency fund that will cover six to 12 months of unexpected expenses. You can build your “rainy day” fund overtime by setting up automatic monthly withdrawals from your checking account. Unfortunately, in the current interest environment, most brick and mortar banks offer 0.1% to 0.2% interest on saving accounts.

Some of the other options to consider are saving account in FDIC-accredited online banks like Discover or Allied Bank, money market account, short term CD, short-term treasuries and municipal bonds.

Maximize your 401k contributions

Many companies now offer 401k plans to their employees as a means to boost employee satisfaction and retention rate. They also provide a matching contribution for up to a certain amount or percentage.

The 401k account contributions are tax deductible and thus decrease your taxable income. Investments grow tax-free. Taxes are due during retirement when money is withdrawn from the account.

Hence, the 401k plan is an excellent platform to set aside money for retirement. The maximum employee contribution for 2016 is $18,000. Your employer can potentially match up to $35,000 for a total joint contribution of $53,000. Companies usually match up to 3% to 5% of your salary.

401K withdrawals

Under certain circumstances, you can take a loan against your 401k or even withdraw the entire amount. Plan participants may decide to take a loan to finance their first home purchase. You can use the funds as last resort income during economic hardship.

In general, I advise against liquidating your 401k unless all other financial options are exhausted. If you withdraw money from your 401k, you will likely pay a penalty. Even if you don’t pay a penalty, you miss out on potential growth through compounded returns.

Read the fine print

Most 401k plans will give you the option to rollover your investments to a tax-deferred IRA account once you leave your employer. You will probably have the opportunity to keep your investments in the current plan. While there are more good reasons to rollover your old 401k to IRA than keep it (a topic worth a separate article), knowing that you have options is half the battle.

Always read the fine print of your employer 401k package. The fact that your company promises to match up to a certain amount of money every year does not mean that the entire match is entirely vested to you. The actual amount that you will take may depend on the number of years of service. For example, some employers will only allow their matching contribution to be fully vested after up to 5 years of service. If you don’t know these details, ask your manager or call HR. It’s a good idea to understand your 401k vesting policy, particularly if you just joined or if you are planning to leave your employer.

In summary, having a 401k is a great way to save for retirement even if your employer doesn’t match or imposes restrictions on the matching contributions. Whatever amount you decide to invest, it is yours to keep. Your money will grow tax-free.

Maximize your Roth IRA

Often neglected, a Roth IRA is another great way to save money for retirement. Roth IRA contributions are made after taxes. The main benefit is that investments inside the account grow tax-free. Therefore there are no taxes due after retirement withdrawals. The Roth IRA does not have any age restrictions, minimum contributions or withdrawal requirements.

The only catch is that you can only invest $5,500 each year and only if your modified adjusted gross income is under $117,000 for single and $184,000 for a couple filing jointly. If you make between $117,000 and $132,000 for an individual or $184,000 and $194,000 for a family filing jointly, the contribution to Roth IRA is possible at a reduced amount.

How to decide between Roth IRA and 401k

Ideally, you want to maximize contributions to both plans.

As a rule of thumb, if you expect to be in a higher tax bracket when you retire then prioritizing Roth IRA contributions is a good move. This allows you to pay taxes on retirement savings now (at your lower taxable income) rather than later.

If you expect to retire at a lower rate (make less money), then invest more in a 401k plan.

Nobody can predict with absolute certainty their income and tax bracket in 20 or 40 years. Life sometimes takes unexpected turns. Therefore the safe approach is to utilize all saving channels. Having a diverse stream of retirement income will help achieve higher security, lower risk and balanced after tax income.

I suggest prioritizing retirement contributions in the following order:

- Contribute in your 401k up to the maximum matching contribution by your employer. The match is free money.

- Gradually build your emergency fund by setting up an automatic withdrawal plan

- Maximize Roth IRA contributions every year, $5,500

- Any additional money that you want to save can go into your 401k plan. You can contribute up to $ 18,000 annually plus $6,000 for individuals over 50.

- Invest all extra residual income in your savings and taxable investment account

About the author: Stoyan Panayotov, CFA is a fee-only financial advisor based in Walnut Creek, CA. His firm Babylon Wealth Management offers fiduciary investment management and financial planning services to individuals and families.

Contact Us