Tag REITs

Market Outlook December 2017

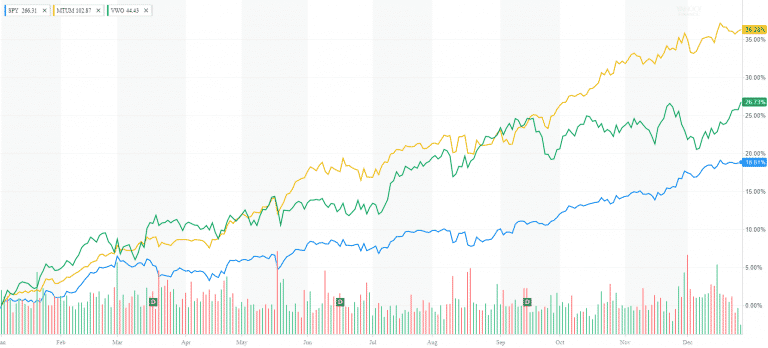

Market Outlook December 2017 As we approach 2018, it‘s time to reconcile the past 365 days of 2017. We are sending off a very exciting and tempestuous year. The stock market is at an all-time high. Volatility is at a…

End of Summer Market Review

End of Summer Market Review Happy Labor Day! Our hearts are with the people of Texas! I wish them to remain strong and resilient against the catastrophic damages of Hurricane Harvey. As someone who experienced Sandy, I can emphasize with…

10 Ways to reduce taxes in your investment portfolio

Successful practices to help you lower taxes in your investment portfolio A taxable investment account is any brokerage or trust account that does not come with tax benefits. Unlike Roth IRA and Tax-Deferred 401k plans, these accounts do not have many…

A Guide to Investing in REITs

On August 31, 2016, S&P 500 will introduce a new sector – Real Estate. Up until now real estate companies, also known as REITs, belonged to the Financial sector. They were in the company of large financial and insurance corporations.…

Contact Us