Inflation is a tax and how to combat it

Inflation is a tax. Let me explain. Inflation reduces the purchasing power of your cash and earnings while simultaneously redistributing wealth to the federal government.

When prices go up, we pay a higher sales tax at the grocery store, restaurants, or gas stations. Even if your employer adjusts your salary with Inflation, the IRS tax brackets may not go up at the same pace. Many critical tax deductions and thresholds are not adjusted for inflation.

For example, the SALT deduction remains at $10,000.

We have a $750,000 cap on total mortgage debt for which interest is tax-deductible. There is a $500,000 cap on tax-free home sales. We also have a $3,000 deduction of net capital losses against ordinary income such as wages.

The income thresholds at which 85% of Social Security payments become taxable aren’t inflation-adjusted and have been $44,000 for joint-filing couples and $34,000 for single filers since 1994

And lastly, even if interest rates on your savings account go up, you still have to pay taxes on your modest interest earnings.

Effectively we ALL will pay higher taxes on our future income

Here are some strategies that can help you combat Inflation.

(Not) keeping cash

Inflation is a tax on your cash. Keeping large amounts of cash is the worst way to protect yourself against Inflation. Inflation hurts savers. Your money automatically loses purchasing power with the rise of Inflation.

Roughly speaking, if this year’s Inflation is 8%, $100 worth of goods and services will be worth $108 in a year from now. Therefore, someone who kept their cash in the checking account will need an extra $8 to buy the same goods and services he could buy for $100 a year ago.

Here is another example. $1,000 in 2000 is worth $1,647 in 2022. If you kept your money in your pocket or a checking account, you could only buy goods and services worth $607 in 2000’s equivalent dollars

I recommend that you keep 6 to 12 months’ worth of emergency funds in your savings account, earning some interest. You can also set aside money for short-term financial goals such as buying a house or paying off debt. If you want to protect yourself from inflation, you need to find a different destination for your extra cash.

Investing in Stocks

Investing in stocks often provides some protection against Inflation. Stock ownership offers a tangible claim over the company’s assets, which will rise in value with Inflation. In inflationary environments, stocks have a distinct advantage over bonds and other investments. Companies that can adjust pricing, whereas bonds, and even rental properties, not so much

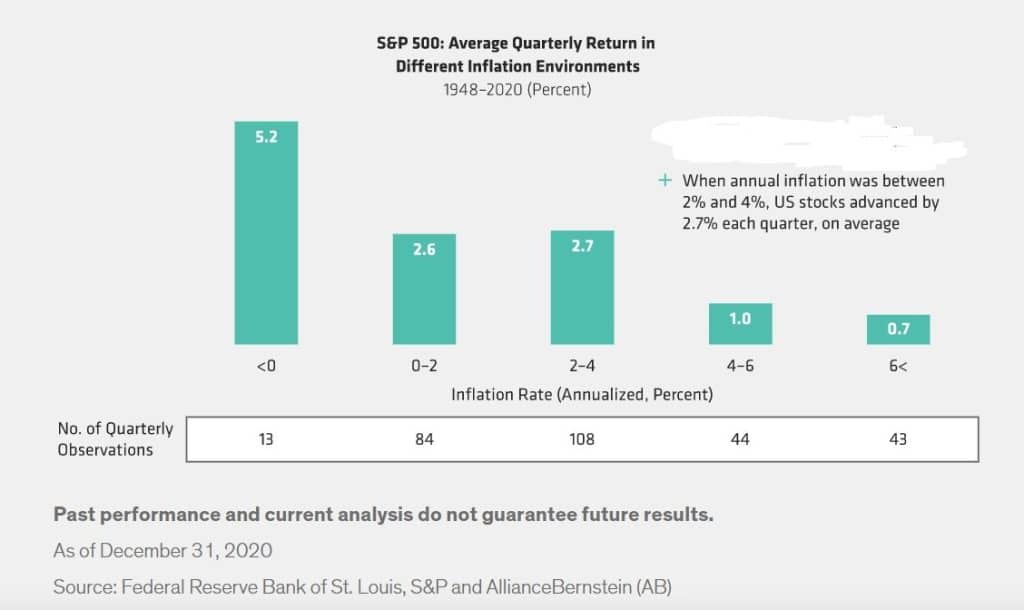

Historical data has shown that equities perform better with inflation rates under 0 and between 0 and 4%.

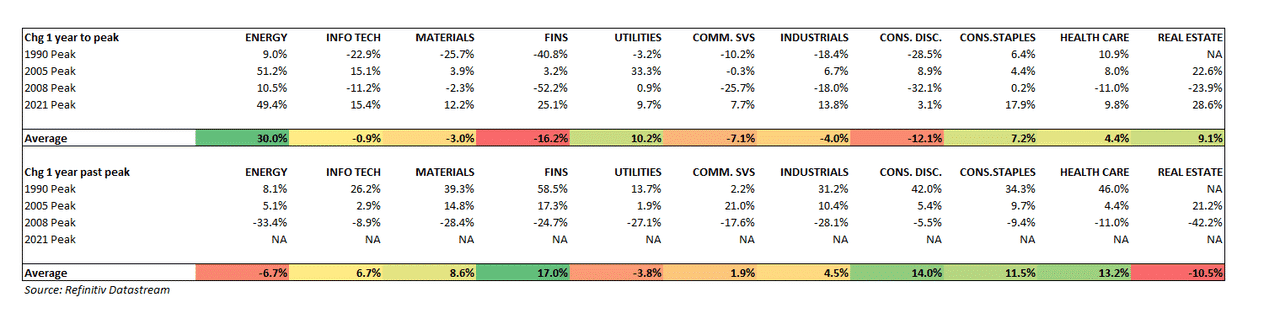

Historically, energy, staples, health care, and utility companies have performed relatively better during high inflation periods, while consumer discretionary and financials have underperformed.

While it might seem tempting to think specific sectors can cope with Inflation better than others, the success rate will come down to the individual companies’ business model. Firms with strong price power and inelastic product demand can pass the higher cost to their customers. Furthermore, companies with strong balance sheets, low debt, high-profit margins, and steady cash flows perform better in a high inflation environment.

You also need to remember that every economic regime is somewhat different. Today, we are less dependent on energy than we were in the 1970s. Corporate leadership is also different. Companies like Apple and Google have superiorly high cash flow margins, low debt, and a smaller physical footprint. Technology plays a more significant role in today’s economy than in the other four inflationary periods.

Investing in Real Estate

Real Estate very often comes up as a popular inflation hedge. In the long-run real estate prices tend to adjust with inflation depending on the location. Investors use real estate to protect against inflation by capitalizing on cheap mortgage interest rates, passing through rising costs to tenants.

However, historical data and research performed the Nobel laureate Robert Shiller show otherwise. Shiller says, “Housing traditionally is not a great investment. It takes maintenance, depreciates, and goes out of style”. On many occasions, it can be subject to climate risk – fires, tornados, floods, hurricanes, and even volcano eruptions if you live on the Big Island. The price of a single house also can be pretty volatile. Just ask the people who bought their homes in 2007, before the housing bubble.

Investors seeking inflation protection with Real Estate must consider their liquidity needs. Real Estate is not a liquid asset class. It takes a longer time to sell it than a stock. Every transaction involves paying fees to banks, lawyers, and real estate agents. Additionally, there are also maintenance costs and property taxes. Rising Inflation will lead to higher overhead and maintenance costs, potential renter delinquency, and high vacancy.

Investing in Gold and other commodities

Commodities and particularly gold, tend to provide some short-term protection against Inflation. However, this is a very volatile asset class. Gold’s volatility, measured by its 50-year standard deviation, is 27% higher than that of stocks and 3.5 times greater than the volatility of the 10-year treasury. Other non-market-related events and speculative trading often overshadow short-term inflation protection benefits.

Furthermore, gold and other commodities are not readily available to retail investors outside the form of ETFs, ETNs, and futures. Buying actual commodities can incur significant transaction and storage costs, making it almost prohibitive for individuals to own them physically.

In recent years the relationship between gold and Inflation has weakened. Gold has become less crucial for the global economy due to monetary policy expansion, benign economic growth, and low and negative interest rates in Japan and the EU.

Having a Roth IRA

If higher Inflation means higher taxes, there is no better tool to lower your future taxes than Roth IRA. I have written a lot about why you need to establish a Roth IRA. Roth IRA is a tax-exempt retirement savings account that allows you to make after-tax dollars. The investments in your Roth IRA grow tax-free, and all your earnings are tax=emept.

If you are a resident of California, the highest possible tax rate you can pay are

- 37% for Federal Income taxes

- 13.3% for State Income taxes

- 2% for Social Security Income tax for income up to $147,000 in 2022

- 35% for Medicare Taxes

- 20% Long-term capital gain tax

- 8% for Net Investment income tax (NIIT) for your MAGI is over $200,000 for singles and $250,000 for married filing jointly

Having a Roth IRA helps you reduce the tax noise on your earnings and improves the tax diversification of your investments

Here is how to increase your Roth contributions depending on your individual circumstances:

- Roth IRA contributions

- Backdoor Roth contributions

- Roth 401k Contributions

- Mega-back door 401k conversions

- Roth conversions from your IRA

Contact Us