Category Personal Finance

The Hidden Costs of Aging: How to Future-Proof Your Retirement Plan

Hidden Costs of Aging. When most people envision retirement, they picture the fun stuff: traveling the world, perfecting their golf swing, or finally having the time to spoil their grandchildren. You diligently calculate how much income you’ll need to cover…

A Physician’s Guide to Student Loans in 2026 and beyond

The Unique Student Debt Burden on Physicians Physicians typically graduate with among the highest levels of student debt of any profession, with average educational debt often exceeding $200,000. This carries implications for career choice, practice setting, burnout risk, specialty selection,…

TSP Contribution Limit for 2026. Empower your savings

TSP contribution limit for 2026. For 2026, several key changes and inflation adjustments have been implemented for the Thrift Savings Plan (TSP) and other retirement accounts. Below is the updated information for the 2026 tax year. TSP Contribution Limit for…

Your 401k contribution limits for 2026. Supercharge your wealth.

401(k) contribution limits for 2026 are $24,500 per person, up from $23,500 in 2025. All 401(k) participants aged 50 and over can make a standard catch-up contribution of $8,000, for a total of $32,500. Under the SECURE 2.0 Act, participants…

Know Your Tax Bracket in 2026

Tax Bracket in 2026. Understanding your 2026 tax brackets is crucial to managing your finances effectively. For the 2026 tax year, the IRS has adjusted income thresholds and standard deductions to account for inflation and new legislative updates under the…

Smart 401(k) moves to make in 2025

Smart 401(k) moves to make in 2025 to grow your retirement savings. Your 401(k) is one of the most effective vehicles for building long-term wealth, and the choices you make today can shape your financial future. As we step into…

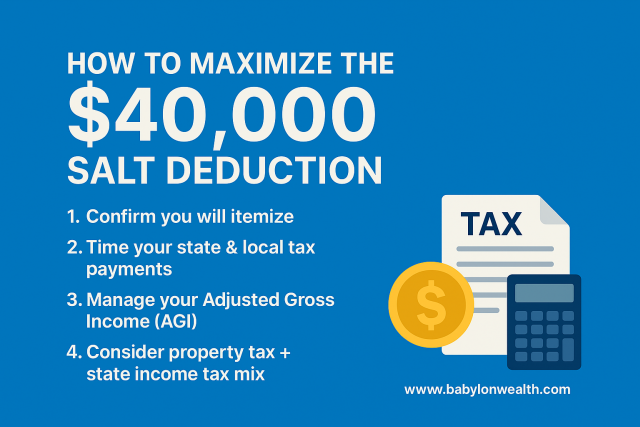

Maximize the $40,000 SALT Deduction: Strategies for High-Tax Households

For many taxpayers, the State and Local Tax (SALT) deduction is one of the most critical factors in determining their overall tax liability. With the cap on this deduction having been temporarily increased to $40,000 (up from the previous $10,000…

Powerful Tax Saving Moves for 2025

Tax Saving moves for 2025. As the 2025 tax season approaches, it’s the perfect time to take stock of your finances and find ways to reduce your tax bill. The Big Beautiful Bill introduced many changes to the taxation of…

The Ultimate Guide to Early Retirement: A Step-by-Step Blueprint

Early retirement is more than a dream—it’s an achievable goal with a disciplined plan. Whether you envision traveling the world, pursuing passions, or simply enjoying freedom from the 9-to-5 grind, this step-by-step blueprint will guide you toward financial independence and…

TSP Contribution Limits for 2025. Empower your savings

TSP contribution limit for 2026 is 23,500 per person. Additionally, all federal employees over the age of 50 can contribute a catch-up of $7,500 per year. Starting in 2025, TSP participants who reached the ages of 60, 61, 62, and…

Your Roth Contribution Limits for 2025. Boost your tax free savings.

The Roth contribution limits for 2025 are $7,000 per person, with an additional $1,000 catch-up contribution for people who are 50 or older. There is no change from 2024. Roth IRA income limits for 2025 Roth IRA contribution limits for…

Your 401k contribution limits for 2025. Empower your wealth.

401k contribution limits for 2025 are $23,500 per person, up from 23,000 in 2024. All 401k participants over 50 can make a catch-up contribution of $7,500, for a total of $31,000. Starting in 2025, 401k participants who are reaching the…

Know Your Tax Bracket in 2025

Understanding your tax brackets for 2025 is crucial in managing your finances effectively and ensuring you make the most of your income. Tax brackets determine the rate at which your income is taxed, and knowing where you fall can help…

What to expect from the stock market in 2025?

As we step into 2025, we will eagerly watch the stock market again, hoping to build on the gains of the past two years. While no one can predict market direction with absolute certainty, a combination of recent market trends,…

Last minute tax savings moves for 2024

Tax Saving moves for 2024. As we approach the end of the year, taxpayers have a valuable opportunity to reassess their financial strategies and explore practical ways to reduce their tax burden. Implementing last-minute tax-saving moves in 2024 maximizes savings…

Five tax-smart ways to plan your legacy

Planning your legacy is more than just drafting a will. It is a profound undertaking beyond the mere distribution of assets. Planning your legacy is about ensuring your assets and values endure for generations. It’s about shaping your impact on…

Tax advantages and benefits of using Health Savings Account

A Health Savings Account (HSA) is a tax-advantaged savings account that individuals can use to set aside funds for qualified medical expenses. HSAs are designed to work together with high-deductible health plans (HDHPs), which are health insurance plans with higher…

10 Essential Money Saving Tips for 2024

10 Essential Money Saving Tips for 2024. It’s 2024. You turned a new chapter of your life. Here is an opportunity to make smart financial decisions and change your future. I have my list of ideas to help you care…

Last minute 401k moves to make in 2023

Last minute 401k moves to make in 2023 to boost your retirement savings. Do you have a 401k? These six 401k moves will help you grow your retirement savings and ensure that you take full advantage of your 401k benefits.…

Retirement Checklist: Your Comprehensive Guide to a Secure Retirement

Retirement is a significant life milestone that requires careful planning and preparation. Whether you’re approaching retirement age or still in the early stages of your career, having a retirement checklist is essential to ensure a financially secure and enjoyable retirement.…

Contact Us