Powerful Tax Saving Moves for 2025

Tax Saving moves for 2025. As the 2025 tax season approaches, it’s the perfect time to take stock of your finances and find ways to reduce your tax bill. The Big Beautiful Bill introduced many changes to the taxation of individuals and businesses. The impact of these changes on your tax return will depend on your individual circumstances. Feel free to reach out if you have any questions.

Implementing these powerful tax-saving moves in 2025 could maximize your tax savings and provide peace of mind as deadlines approach. From optimizing retirement contributions to leveraging deductions, credits, and investment opportunities, proactive planning can lead to substantial benefits. Whether you’re an employee, business owner, or retiree, thoughtful planning can make a big difference. Here are ten smart tax-saving moves to consider this year.

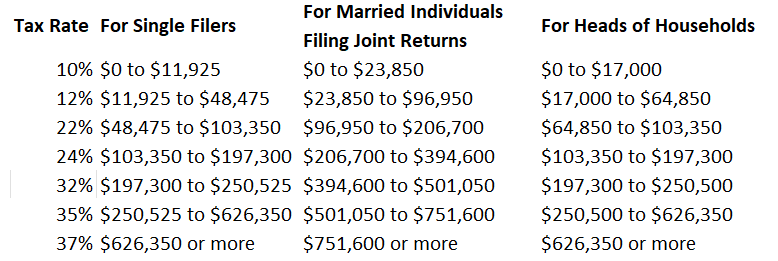

1. Know your 2025 tax bracket

The first step in managing your taxes is knowing your tax bracket. 2025 federal tax rates fall into the following brackets, depending on your taxable income and filing status. Knowing where you land on the tax scale can help you make informed decisions, especially when you plan to earn additional income, exercise stock options, or receive RSUs.

Tax Brackets for 2025

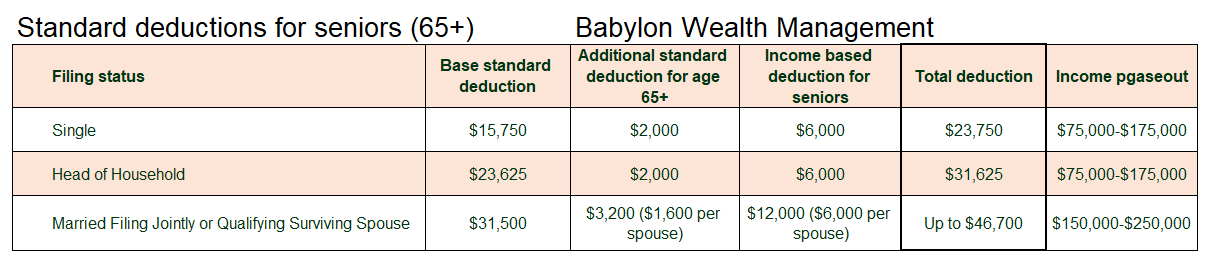

2. Decide to Itemize or use the Standard Deduction

The standard deduction is a specific dollar amount that allows you to reduce your taxable income. Nearly 90% of all tax filers use the standard deduction instead of itemizing. It makes the process a lot simpler for many Americans. However, in some circumstances, your itemized deductions may exceed the standard deduction, allowing you to lower your tax bill even further.

- Single or Married Filing Separately: $15,750

- Married Filing Jointly or Qualifying Surviving Spouse: $31,500

- Head of Household: $23,625

Additional tax deduction for seniors

| Senior cisitzend over the age of 65 are eligible for an additional standard deduction. |

- Additional Standard Deduction for Married Seniors – $1,600 per person

- Additional Standard Deduction for Unmarried Seniors – $2,000 per person

Important: There’s also a temporary bonus deduction for those age 65+ introduced under the Big Beautiful Bill of 2025. The deduction can add up to $6,000 for single filers or a head of household (or $12,000 for married filing jointly. To claim the new deduction for seniors, you must meet the following criteria:

- Be 65 or older by the end of the tax year.

- Have a work-authorized Social Security number.

- Use any Filing Status other than Married Filing Separately.

- The phaseout range is $75,000 to $175,000 for those filing as Single.

- The phaseout range is $150,000- $250,000 for Married Filing Jointly.

Here is a summary of all available deductions for seniors.

SALT Deduction

The State and Local Tax (SALT) deduction allows taxpayers to deduct certain state and local taxes they have paid when filing their federal income tax returns. Taxpayers can claim the SALT deduction only if they choose to itemize their deductions instead of taking the standard deduction.

The One Big Beautiful Bill Act (OBBBA) increased the cap for the tax years 2025 through 2029.

- 2025 cap: $40,000 for most filers ($20,000 for married filing separately (MFS)).

- 2025 income phaseout: The cap is reduced for taxpayers with a modified adjusted gross income (MAGI) between $500,000 and $600,000 ($250,000 and $300,000 for married filing separately.

- Income over $600,000 MAGI ($300,000 MFS): For any income at or above this level, the SALT deduction reverts to the previous $10,000 cap ($5,000 MFS)

- The phaseout provision creates a narrow income band that some tax professionals are calling a “SALT torpedo”. This happens because a slight increase in income can lead to a steep reduction in the available deduction, which effectively raises the marginal tax rate for taxpayers in that income range.

- Sunset: The cap will revert to the previous $10,000 ($5,000) limit for tax year 2030 and beyond.

3. Maximize your retirement contributions

You can lower taxes by contributing to a retirement plan. Most contributions to qualified retirement plans are tax-deductible, which reduces your tax bill.

- For employees: 401(k), 403 (b), 457, and TSP. The maximum contribution to qualified employee retirement plans for 2025 is $23,500. If you are 50 or older, you can contribute an additional $7,500.

- For business owners – SEP IRA, Solo 401 (k), and Defined Benefit Plan. Business owners can contribute to a SEP IRA, a Solo 401(k), and a Defined Benefit Plan to maximize their retirement savings and lower their tax bills. The maximum contribution to SEP-IRA and Solo 401 (k) in 2025 is $70,000 or $77,500 if you are 50 and older.

If you own a SEP IRA, you can contribute up to 25% of your business wages.

In a solo 401 (k) plan, you can contribute as an employee and an employer. The employee contribution is subject to a $23,500 limit, plus a $7,500 catch-up contribution. The employer match is limited to 25% of your compensation, up to $70,000, or $77,000 if you are older than 50. In many cases, the solo 401 (k) plan can allow you to save more than a SEP IRA.

A defined Benefit Plan is an option for high-income earners who want to save more aggressively for retirement, beyond the SEP-IRA and 401(k) limits. The DB plan uses actuary rules to calculate your annual contribution limits based on your age and compensation. All contributions to your defined benefit plan are tax-deductible, and the earnings grow tax-free.

4. Roth conversion

Transferring investments from a Traditional IRA or 401(k) plan to a Roth IRA is called a Roth Conversion. It allows you to switch from tax-deferred to tax-exempt retirement savings.

The conversion amount is taxable for income purposes. The good news is that even though you will pay more taxes this tax year, the conversion may save you much more money in the long run.

If you believe your taxes will go up in the future, a Roth Conversion could be a very effective way to manage your future taxes.

5. Contribute to a 529 plan

The 529 plan is a tax-advantaged state-sponsored investment plan allowing parents to save for their children’s future college expenses. 529 plan works similarly to the Roth IRA. You make post-tax contributions. Your investment earnings grow free from federal and state income tax if you use them to pay for qualified educational expenses. The 529 plan has a distinct tax advantage compared to a regular brokerage account, as you will never pay taxes on your dividends and capital gains.

Over 30 states offer a full or partial tax deduction or a credit on your 529 contributions. You can find the complete list here. Your 529 contributions can significantly lower your state tax bill if you live in these states.

6. Make a donation

Donations to charities, churches, and various non-profit organizations are tax-deductible. You can support your favorite cause while also lowering your tax bill. Your contributions can be in cash, household goods, appreciated assets, or directly from your IRA distributions.

Charitable donations are tax-deductible only when you itemize your tax return. If you make small contributions throughout the year, you might be better off taking the standard deduction.

If itemizing your taxes is crucial, you might want to consolidate your donations into a single calendar year. So, instead of making multiple charitable contributions over the years, you can give one large donation every few years.

Qualified charitable distribution (QCD)

If you’re 70½ or older, you can donate up to $108,000 for tax year 2025 to a charity directly from your IRA or a 401 (k) plan using a QCD. (If both spouses qualify, you each can donate up to the limit.) You won’t be taxed on the distribution or receive a tax deduction for the donation, but you can use your gift to satisfy all or part of your RMD without adding to your taxable income.

7. Tax-loss harvesting

The stock market is volatile. If you are holding stocks and other investments that dropped significantly in 2025, you can consider selling them. Selling losing investments to reduce your tax liability is known as tax-loss harvesting. It works for capital assets outside retirement accounts (401 (k), Traditional IRA, and Roth IRA). Capital assets may include real estate, cryptocurrency, cars, gold, stocks, bonds, and any investment property not for personal use.

The IRS allows you to use capital losses to offset capital gains. You can deduct the difference as a loss on your tax return if your capital losses exceed your capital gains. This loss is limited to $3,000 annually or $1,500 if married and filing a separate return. Furthermore, you can carry forward your capital losses to offset future gains.

8. Prioritize long-term over short-term capital gains

Another way to lower your tax bill when selling assets is to prioritize long-term over short-term capital gains. The current tax code benefits investors who hold their assets for more than one calendar year. Long-term investors receive a preferential tax rate on their gains. At the same time, investors with short-term capital gains will pay taxes at their ordinary income tax level.

| FILING STATUS | 0% RATE | 15% RATE | 20% RATE |

|---|---|---|---|

| Single | Up to $48,350 | $48,351 – $533,400 | Over $533,400 |

| Married filing jointly | Up to $96,700 | $96,701 – $600,050 | Over $600,050 |

| Married filing separately | Up to $48,350 | $48,351 – $300,000 | Over $300,000 |

| Head of household | Up to $64,750 | $64,751 – $566,700 | Over $566,700 |

Source: Internal Revenue Service

9. Contribute to FSA

With healthcare costs constantly increasing, you can use a Flexible Spending Account (FSA) to cover your medical bills and lower your tax bill.

Flexible Spending Account (FSA)

A Flexible Spending Account (FSA) is a tax-advantaged savings account offered through your employer. The FSA allows you to save pretax dollars to cover medical and dental expenses for yourself and your dependents.

The maximum contribution for 2025 is $3,300 per person. If married, your spouse can save an additional $3,300, bringing the total to $6,400 per family. Some employers offer a matching FSA contribution for up to $500. Typically, you should use your FSA savings by the end of the calendar year. However, for 2025, the maximum carryover amount is $660, which you can roll over for the following calendar year.

Dependent Care FSA (DC-FSA)

A Dependent Care FSA is a pretax benefit account that you can use to pay for eligible dependent care services, such as preschool, summer day camp, before or after-school programs, and child or adult daycare. You can reduce your tax bill while taking care of your children and loved ones, while you continue working.

The American Rescue Plan Act (ARPA) raised the pretax contribution limits for dependent care flexible spending accounts (DC-FSAs) for 2025. The maximum contribution limit is $5,000 for married couples filing jointly or single parents filing as head of household.

10. Contribute to a Health Savings Account (HSA)

A Health Savings Account (HSA) is an investment account for individuals under a High Deductible Health Plan (HDHP) that allows you to save on a pretax basis to pay for eligible medical expenses.

Keep in mind that the HSA has three distinct tax advantages.

- All HSA contributions are tax-deductible and will lower your tax bill.

- Your investments grow tax-free. You will not pay taxes on dividends, interest, and capital gains.

- You don’t pay taxes on those withdrawals if you use the account for eligible medical expenses.

The qualified High Deductible Plan typically covers only preventive services before the deductible. To qualify for the HSA, the HDHP should have a minimum deductible of $1,600 for an individual and $3,200 for a family. Additionally, your HDHP must have an out-of-pocket maximum of $8,050 for single coverage or $16,100 for family coverage.

The maximum HSA contributions for 2025 are $4,300 for individual coverage and $8,550 for family coverage. HSA participants of age 55 or older can contribute an additional $1,000 as a catch-up contribution. Unlike the FSA, the HSA doesn’t have a spending limit, and you can carry over the savings in the next calendar year.

11. Defer or accelerate income

Is 2025 shaping up to be a high-income year for you? Perhaps you can defer some of your income from this calendar year into 2026. This move will allow you to reduce or delay higher income taxes. Even though it’s not always possible to defer wages, you might be able to postpone a large bonus, royalty, capital gains, option exercise, or one-time payment. Remember, it only makes sense to defer income if you expect to be in a lower tax bracket next year.

On the other hand, if you expect to be in a higher tax bracket next year, you may consider taking as much income as possible in 2025.

Contact Us