TSP Contribution Limit for 2026. Empower your savings

TSP contribution limit for 2026. For 2026, several key changes and inflation adjustments have been implemented for the Thrift Savings Plan (TSP) and other retirement accounts. Below is the updated information for the 2026 tax year.

TSP Contribution Limit for 2026

The IRS has increased the annual elective deferral limit due to cost-of-living adjustments. These limits apply to the combined total of Traditional (pre-tax) and Roth (after-tax) contributions.

The TSP contribution limit for 2026 is $ 24,500 per person. Additionally, all federal employees over the age of 50 can contribute a catch-up of $8,500 per year. Maximum Annual Limit (Employee + Employer) si $72,000

In 2026, TSP participants who reach the ages of 60, 61, 62, and 63 can contribute an additional $11,500, rather than the lower $8,000 limit.

For participants who contribute to both a civilian and a uniformed services TSP account during the year, the elective deferral and catch-up contribution limits apply to the combined amounts of traditional (tax-deferred) and Roth contributions in both accounts.

Members of the uniformed services, receiving tax-exempt pay (i.e., pay that is subject to the combat zone tax exclusion), your contributions from that pay will also be tax-exempt. Your total contributions from all types of pay must not exceed the combined limit of $72,000 per year.

What is TSP?

A thrift saving plan is a federal retirement plan that allows federal employees to make contributions to their retirement. Moreover, this retirement plan is one of the easiest and most effective ways to save for retirement. As a federal employee, you can automatically contribute to your TSP directly through your paycheck. You can choose the percentage of your salary to contribute to your retirement savings. TSP offers multiple investment options, including stocks, fixed income, and lifecycle funds.

Additionally, most agencies offer a TSP that matches up to a certain percentage. In most cases, you must participate in the plan to get the government match. For more information about investment options in your TSP account, check my article – “Grow your retirement savings with the Thrift Savings Plan.”

Who is Eligible to Participate in the TSP?

Most employees of the United States Government are eligible to participate in the Thrift Savings Plan. You qualify if you are:

- Federal Employees’ Retirement System (FERS) employee (started on or after January 1, 1984)

- Civil Service Retirement System (CSRS) employee (started before January 1, 1984, and did not convert to FERS)

- Member of the uniformed services (active duty or Ready Reserve)

- A Civilian in certain other categories of Government service

Tax-deferred TSP

Most federal employees typically choose to make tax-deferred TSP contributions. These contributions are tax-deductible. They will lower your tax bill for the current tax year. Your investments will grow on a tax-deferred basis. Therefore, you will only owe federal and state taxes when you start withdrawing your savings.

Expanded “Super” Catch-Up

TSP Participants who reach ages 60, 61, 62, or 63 during the calendar year remain eligible for the higher catch-up limit of $11,250. This allows a total personal contribution of $35,750 ($24,500 + $11,250). Note that once you turn 64, your catch-up limit returns to the standard $8,000.

Roth TSP

Roth TSP contributions are pretax. It means that you will pay all federal and state taxes before making your contributions. The advantage of Roth TSP is that your retirement savings will grow tax-free. As long as you keep your money until retirement, you will withdraw your gains tax-free. It’s a great alternative for young professionals and workers in a low tax bracket.

Mandatory Roth Catch-Up for High Earners

A major provision of the SECURE 2.0 Act takes effect on January 1, 2026. If your wages from the previous year (2025) exceeded $150,000, any catch-up contributions you make in 2026 must be Roth.

- What this means: You cannot make pre-tax (Traditional) catch-up contributions if you hit this income threshold. Your payroll office will automatically transition any catch-up amounts to your Roth balance.

Roth In-Plan Conversions

Starting in early 2026, the TSP is scheduled to introduce a feature allowing participants to convert existing Traditional (pre-tax) balances into Roth (after-tax) balances within the plan

TSP Matching

Federal agencies can make a matching contribution up to the combined limit of 72,000 or $80,000, including the catch-up contribution. If you contribute the maximum allowed amount, your agency match cannot exceed $47,500 in 2026.

If you are an eligible FERS or BRS employee, you will receive matching contributions from your agency based on your regular employee contributions. Unlike most private companies, matching contributions are not subject to vesting requirements.

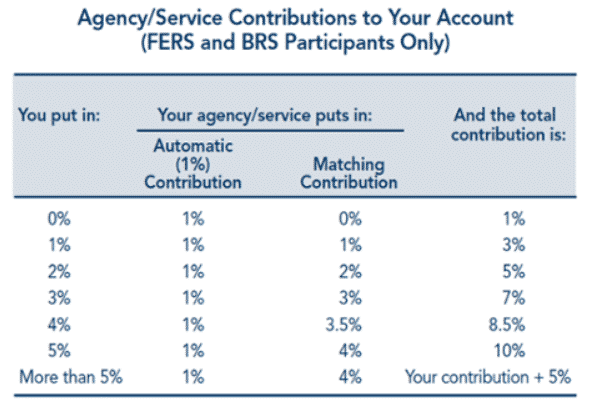

FERS or BRS participants receive matching contributions on the first 5% of their salary contributed each pay period. The first 3% of your contribution will be matched dollar-for-dollar. The next 2% will be matched at 50 cents on the dollar. Contributions above 5% of your salary will not be matched.

Consider contributing at least 5% of your base salary to your TSP account to receive the full matching contribution.

Matching schedule

Opening your TSP account

FERS Employees

If you are a federal employee hired after July 31, 2010, your agency has automatically enrolled you in the TSP. By default, 3% of your base salary will be deducted from your paycheck each pay period and deposited in the traditional balance of your TSP account. If you decide, you have to make an election to change or stop your contributions.

If you are a FERS employee who started before August 1, 2010, you already have a TSP account with 1% automatic contributions accruing. In addition, you can make contributions to your account from your pay and receive additional matching contributions.

CSRS Employees

If you are a Federal civilian employee who started before January 1, 1984, your agency will establish your TSP account after you make a contribution election using your agency’s election system.

BRS Members of the Uniformed Services

Members of the uniformed services who began serving on or after January 1, 2018, will automatically enroll in the TSP after serving 60 days. By default, 3% of your basic pay is deducted from your paycheck.

Work with Babylon Wealth Management

At Babylon Wealth Management, we specialize in helping federal employees navigate the unique complexities of their benefits package. With over a decade of experience and a deep focus on tax-efficient strategies, we ensure your Thrift Savings Plan (TSP), FERS/CSRS pension, and Social Security work in harmony to fund your ideal retirement.

We don’t just manage assets; we provide a clear roadmap to ensure you never leave money on the table – from capturing your full agency match to protecting your legacy.

Contact Us