Tag 529 Plan

Saving for college with a 529 plan

What is a 529 plan? The 529 plan is a tax-advantaged state-sponsored investment plan that allows parents to save for their children’s college expenses. In the past twenty years, college expenses have skyrocketed exponentially, putting many families in difficult situation.…

Tax Saving Moves for 2023

1. Know your tax bracket The first step in managing your taxes is knowing your tax bracket. 2023 federal tax rates fall into the following brackets depending on your taxable income and filing status. Knowing where you land on the…

Tax Saving Strategies for 2022

As we approach the end of 2022, I am sharing my favorite list of tax-saving ideas to help you lower your tax bill for 2022. In my experience, the US tax rules change frequently. 2022 was no exception. 2022 has…

Tax Saving Ideas for 2021

As we approach the end of 2021, I am sharing my favorite list of tax-saving ideas that can help you lower your tax bill for 2021. In my practice, In the US tax rules change frequently. 2021 was no exception.…

Tax Saving Moves for 2020

As we approach the end year, we share our list of tax-saving moves for 2020. 2020 has been a challenging and eventful year. The global coronavirus outbreak changed the course of modern history. The Pandemic affected many families and small…

12 End of Year Tax Saving Tips

As we approach the close of 2019, we share our list of 12 end of year tax saving tips. Now is a great time to review your finances. You can make several smart and simple tax moves that can help…

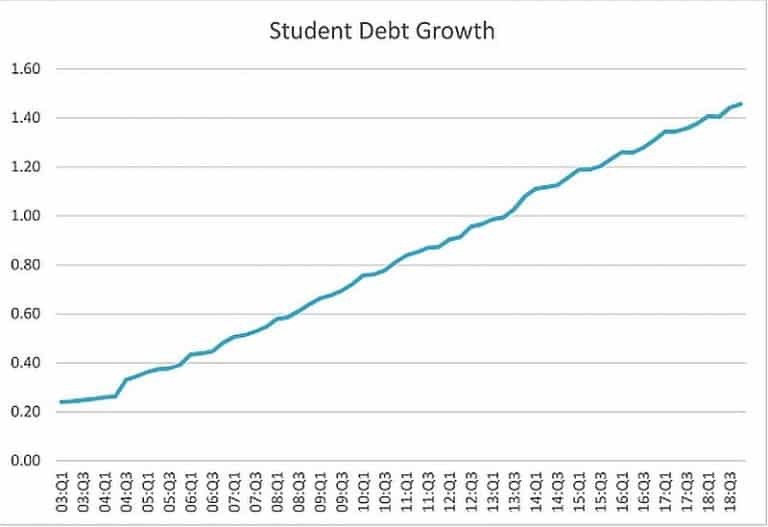

Solving the student debt crisis

The looming student debt crisis As a financial advisor working with many young families, I am regularly discussing college planning. Many of my clients want to help their children with the constantly growing college tuition. Currently, the amount of US…

A financial checklist for young families

A financial checklist for young families…..Many of my clients are young families looking for help to build their wealth and improve their finances. We typically discuss a broad range of topics from buying a house, saving for retirement, savings for…

9 Smart Tax Saving Strategies for High Net Worth Individuals

The Tax Cuts and Jobs Act (TCJA) voted by Congress in late 2017 introduced significant changes to the way high net worth individuals and families file and pay their taxes. The key changes included the doubling of the standard deduction to $12,000…

Contact Us