Tax Saving Moves for 2020

As we approach the end year, we share our list of tax-saving moves for 2020. 2020 has been a challenging and eventful year. The global coronavirus outbreak changed the course of modern history. The Pandemic affected many families and small businesses. The stock market crashed in March, and It had a full recovery in just a few months.

With so many changes, now is a great time to review your finances. You can make a few smart and simple tax moves that can lower your tax bill and increase your tax refund.

Whether you file taxes yourself or hire a CPA, it is always better to be proactive. If you expect a large tax bill or your financials have changed substantially, talk to your CPA. Start the conversation today. Don’t wait until the last moment. Being ahead of the curve will help you make well-informed decisions without the stress of tax deadlines.

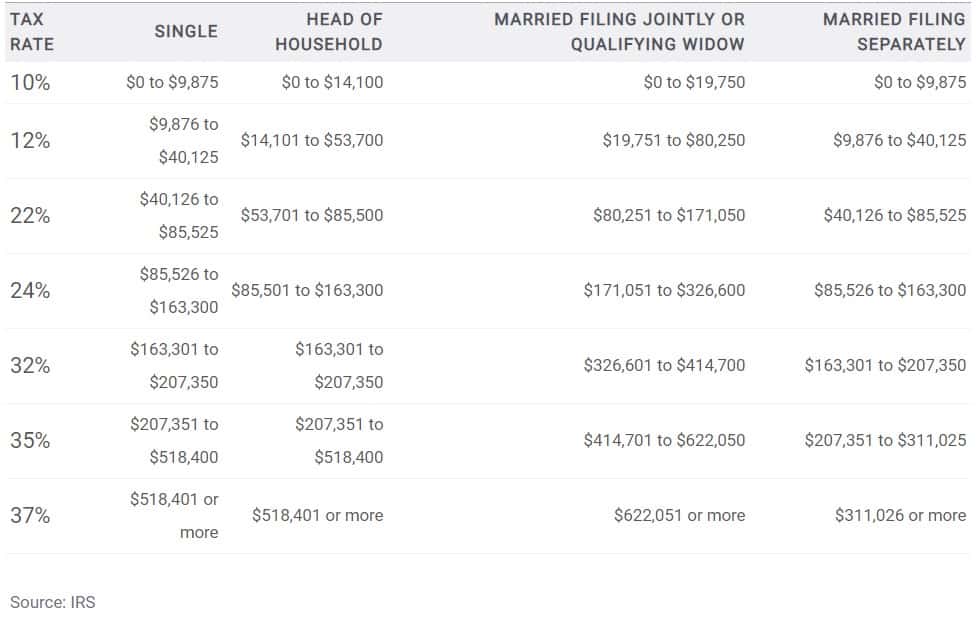

1. Know your tax bracket

The first step of mastering your taxes is knowing your tax bracket. 2020 is the third year after the TCJA took effect. One of the most significant changes in the tax code was introducing new tax brackets.

Here are the tax bracket and rates for 2020.

2. Decide to itemize or use a standard deduction

Another recent change in the tax law was the increase in the standard deduction. The standard deduction is a specific dollar amount that allows you to reduce your taxable income. As a result of this change, nearly 90% of all tax filers will take the standard deduction instead of itemizing. It makes the process a lot simpler for many Americans. Here are the values for 2020:

| Filing status | 2020 tax year |

| Single | $12,400 |

| Married, filing jointly | $24,800 |

| Married, filing separately | $12,400 |

| Head of household | $18,650 |

3. Maximize your retirement contributions

You can save taxes by contributing to a retirement plan. Most contributions to qualified retirement plans are tax-deductible and will lower your tax bill.

- For employees – 401k, 403b, 457, and TSP. The maximum contribution to qualified employee retirement plans for 2020 is $19,500. If you are at the age of 50 or older, you can contribute an additional $6,500.

- For business owners – SEP IRA, Solo 401k, and Defined Benefit Plan. Business owners can contribute to SEP IRA, Solo 401k, and Defined Benefit Plans to maximize your retirement savings and lower your tax bill. The maximum contribution to SEP-IRA and Solo 401k in 2020 is $57,000 or $63,500 if you are 50 and older.

If you own SEP IRA, you can contribute up to 25% of your business wages.

In a solo 401k plan, you can contribute as both an employee and an employer. The employee contribution is subject to a $19,500 limit plus a $6,500 catch-up. The employer match is limited to 25% of your compensation for a maximum of $37,500. In many cases, the solo 401k plan can allow you to save more than SEP IRA.

Defined Benefit Plans is an option for high-income earners who want to save more aggressively for retirement above the SEP-IRA and 401k limits. The DB plan uses actuary rules to calculate your annual contribution limits based on your age and compensation. All contributions to your defined benefit plan are tax-deductible, and the earnings grow tax-free.

4. Convert to Roth IRA

Transferring investments from a Traditional IRA or 401k plan to a Roth IRA is known as Roth Conversion. It allows you to switch from tax-deferred to tax-exempt retirement savings.

The conversion amount is taxable for income purposes. The good news is that even though you will pay more taxes in the current year, the conversion may save you a lot more money in the long run.

If you believe that your taxes will go up in the future, Roth Conversion could be a very effective way to manage your future taxes.

5. Contribute to a 529 plan

The 529 plan is a tax-advantaged state-sponsored investment plan, allowing parents to save for their children’s future college expenses. 529 plan works similarly to the Roth IRA. You make post-tax contributions. Your investment earnings grow free from federal and state income tax if you use them to pay for qualified educational expenses. Compared to a regular brokerage account, the 529 plan has a distinct tax advantage as you will never pay taxes on your dividends and capital gains.

Over 30 states offer a full or partial tax deduction or a credit on your 529 contributions. You can find the full list here. If you live in any of these states, your 529 contributions can significantly lower your state tax bill.

6. Make a donation

Donations to charities, churches, and various non-profit organizations are tax-deductible. You can support your favorite cause by giving back and lower your tax bill at the same time.

However, due to the new tax code changes, donations are tax-deductible only when you itemize your tax return. If you make small contributions throughout the year, you will be better off taking the standard deduction.

If itemizing your taxes is crucial for you, you might want to consolidate your donations in one calendar year. So, instead of making multiple charitable contributions over the years, you can give one large donation every few years.

7. Sell losing investments

2020 has been turbulent for the stock market. If you are holding stocks and other investments that dropped significantly in 2020, you can consider selling them. The process of selling losing investments to reduce your tax liability is known as tax-loss harvesting. It works for capital assets held outside retirement accounts (401k, Traditional IRA, and Roth IRA). Capital assets may include real estate, cars, gold, stocks, bonds, and any investment property, not for personal use.

The IRS allows you to use capital losses to offset capital gains. If your capital losses are higher than your capital gains, you can deduct the difference as a loss on your tax return. This loss is limited to $3,000 per year or $1,500 if married and filing a separate return.

8. Prioritize long-term over short-term capital gains

Another way to lower your tax bill when selling assets is to prioritize long-term over short-term capital gains. The current tax code benefits investors who keep their assets for more than one calendar year. Long-term investors receive a preferential tax rate on their gains. While investors with short-term capital gains will pay taxes at their ordinary income tax level

Here are the long-term capital gain tax brackets for 2020:

| Long-Term Capital Gains Tax Rate | Single Filers (Taxable Income) | Married Filing Separately |

|---|---|---|

| 0% | $0-$40,000 | $0-$40,000 |

| 15% | $40,000-$441,450 | $40,000-$248,300 |

| 20% | Over $441,550 | Over $248,300 |

High-income earners will also pay an additional 3.8% net investment income tax.

9. Contribute to FSA and HSA

With healthcare costs always on the rise, you can use a Flexible Spending Account (FSA) or a Health Savings Account (HSA) to cover your medical bills and lower your tax bill.

Flexible Spending Account (FSA)

A Flexible Spending Account (FSA) is tax-advantaged savings account offered through your employer. The FSA allows you to save pre-tax dollars to cover medical and dental expenses for yourself and your dependents. The maximum contribution for 2020 is $2,750 per person. If you are married, your spouse can save another $2,750 for a total of $5,500 per family. Some employers offer a matching FSA contribution for up to $500. Typically, it would help if you used your FSA savings by the end of the calendar year. However, the IRS allows you to carry over up to $500 balance into the new year.

Dependent Care FSA (CSFSA)

A Dependent Care FSA (CSFSA) is a pre-tax benefit account that you can use to pay for eligible dependent care services, such as preschool, summer day camp, before or after school programs, and child or adult daycare. It’s an easy way to reduce your tax bill while taking care of your children and loved ones while you continue to work. The maximum contribution limit for 2020 for an individual who is married but filing separately is $2,500. For married couples filing jointly or single parents filing as head of household, the limit is $5,000.

Health Savings Account (HSA)

A Health Savings Account (HSA) is an investment account for individuals under a High Deductible Health Plan (HDHP) that allows you to save money on a pre-tax basis to pay for eligible medical expenses. The qualified High Deductible Plan typically covers only preventive services before the deductible. To qualify for the HSA, the HDHP should have a minimum deductible of $1,400 for an individual and $2,800 for a family. Additionally, your HDHP must have an out-of-pocket maximum of up to $6,900 for one-person coverage or $13,800 for family.

The maximum contributions in HSA for 2020 are $3,550 for individual coverage and $7,100 for a family. HSA participants who are 55 or older can contribute an additional $1,000 as a catch-up contribution. Unlike the FSA, the HSA doesn’t have a spending limit, and you can carry over the savings in the next calendar year.

Keep in mind that the HSA has three distinct tax advantages. First, all HSA contributions are tax-deductible and will lower your tax bill. Second, you will not pay taxes on dividends, interest, and capital gains. Third, if you use the account for eligible expenses, you don’t pay taxes on those withdrawals.

10. Defer income

Is 2020 shaping to be a high income for you? Perhaps, you can defer some of your income from this calendar year into 2021 and beyond. This move will allow you to delay some of the income taxes coming with it. Even though it’s not always possible to defer wages, you might be able to postpone a large bonus, royalty, or one-time payment. Remember, it only makes sense to defer income if you expect to be in a lower tax bracket next year.

On the other hand, if you expect to be in a higher tax bracket tax year next year, you may consider taking as much income as possible in 2020.

11. Skip RMDs

Are you taking the required minimum distributions (RMD) from your IRA or 401k plan? The CARES Act allows retirees to skip their RMD in 2020. If you don’t need the extra income, you can skip your annual distribution. This move will lower your taxes for 2020 and may cut your future Medicare cost.

12. Receive employee retention tax credit for eligible businesses

The CARES Act granted employee retention credits for eligible businesses affected by the Coronavirus pandemic. The credit amount equals 50% of eligible employee wages paid by an eligible employer in a 2020 calendar quarter. The credit is subject to an overall wage cap of $10,000 per eligible employee.

Qualifying businesses must fall into one of two categories:

- The employer’s business is fully or partially suspended by government order due to COVID-19 during the calendar quarter.

- The employer’s gross receipts were below 50% of the comparable quarter in 2019. Once the employer’s gross receipts went above 80% of a comparable quarter in 2019, they no longer qualify after the end of that quarter.

Contact Us