Category College Planning

Tax Saving Moves for 2020

As we approach the end year, we share our list of tax-saving moves for 2020. 2020 has been a challenging and eventful year. The global coronavirus outbreak changed the course of modern history. The Pandemic affected many families and small…

12 End of Year Tax Saving Tips

As we approach the close of 2019, we share our list of 12 end of year tax saving tips. Now is a great time to review your finances. You can make several smart and simple tax moves that can help…

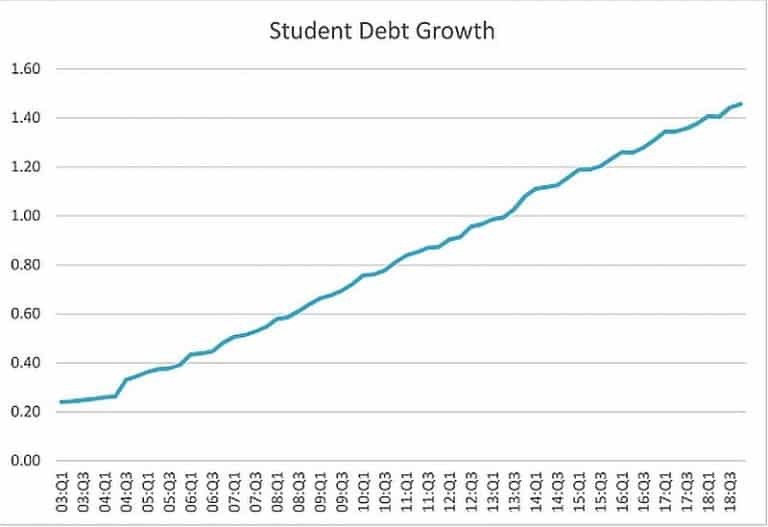

Solving the student debt crisis

The looming student debt crisis As a financial advisor working with many young families, I am regularly discussing college planning. Many of my clients want to help their children with the constantly growing college tuition. Currently, the amount of US…

Savings for college with a 529 plan

What is a 529 plan? A 529 plan is a tax-advantaged, state-sponsored investment plan designed to help families save for a beneficiary’s education expenses. Originally focused on college, these plans have evolved significantly, becoming one of the most flexible tools…

Contact Us