Tag ETFs

Top 5 Dividend Growth ETFs

Dividend growth ETFs offer a convenient and diversified way to invest in companies that consistently grow their dividends. Certainly, dividend-paying stocks provide a predictable stream of cash flows to investors looking for extra income. Companies that steadily grow their dividends year…

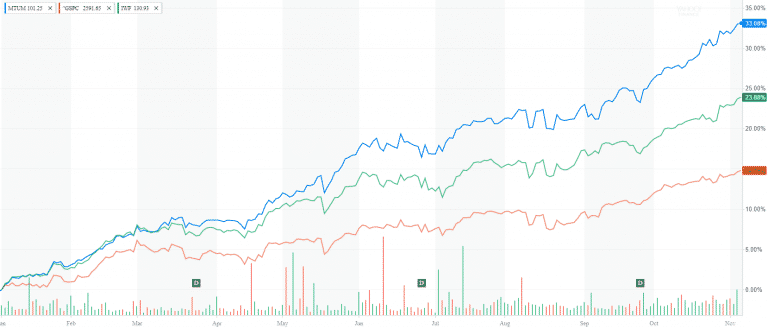

The Rise of Momentum Investing

The Rise of Momentum Investing While the momentum theory has been around for two decades, we had to wait until 2017 to see the rise of momentum investing. The largest momentum ETF (MTUM) is up 35% YTD. And unless something…

5 Myths and One True Fact about passive investing

The passive investing in ETFs and index funds has experienced a massive influx of money in the past ten years. The US ETF market is quickly approaching $3 trillion in assets under management. As of March 29, 2017, the total…

MLP Investing – Risks and benefits

MLP investing is popular among retirees and income-seeking investors. In this article, we will break down the benefits, risks and tax implications of investing in MLPs. What is an MLP? Managed Limited Partnerships (MLPs) have grown in popularity in the…

Investing in Small Cap Stocks

Small cap stocks are an important part of a diversified investment portfolio. They had provided high historical return and diversification, which are key factors in the portfolio management process. Many flagship companies started as small businesses in a local market…

10 Ways to reduce taxes in your investment portfolio

Successful practices to help you lower taxes in your investment portfolio A taxable investment account is any brokerage or trust account that does not come with tax benefits. Unlike Roth IRA and Tax-Deferred 401k plans, these accounts do not have many…

A Guide to Investing in REITs

On August 31, 2016, S&P 500 will introduce a new sector – Real Estate. Up until now real estate companies, also known as REITs, belonged to the Financial sector. They were in the company of large financial and insurance corporations.…

A beginner’s guide to ETF Investing

What is an ETF? ETF stands for an exchange-traded fund. The fund is a passively managed marketable security that tracks an index, a commodity, or a pool of bonds. ETFs trade on the stock exchange, and their price fluctuate throughout the…

Contact Us