What Successful Investors Do During Market Stress

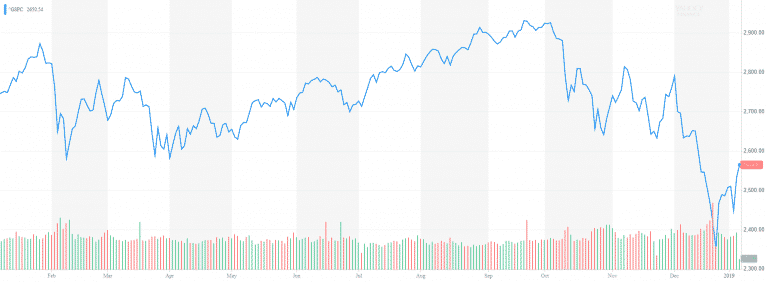

In the world of investing, there is a distinct difference between “market noise” and “market signal.” Today, as headlines are dominated by the conflict in Iran and the resulting volatility in energy markets, that distinction has never been more critical.…