Achieving tax alpha and higher after tax returns on your investments

What is tax alpha?

Tax Alpha is the ability to achieve an additional return on your investments by taking advantage of a wide range of tax strategies as part of your comprehensive wealth management and financial planning. As you know, it is not about how much you make but how much you keep. And tax alpha measures the efficiency of your tax strategy and the incremental benefit to your after-tax returns.

Retirement CalculatorWhy is tax alpha important to you?

The US has one of the most complex tax systems in the world. Navigating through all the tax rules and changes can quickly turn into a full-time job. Furthermore, the US budget deficit is growing exponentially every year. The government expenses are rising. The only way to fund the budget gap is by increasing taxes, both for corporations and individuals.

Obviously, our taxes pay our teachers, police officers, and firefighters, fund essential services, build new schools and fix our infrastructure. Our taxes help the world around us humming. However, there will be times when taxes become a hurdle in your decision process. Taxes turn into a complex web of rules that is hard to understand and even harder to implement.

Achieving tax alpha is critical whether you are a novice or seasoned investor sitting on significant investment gains. Making intelligent and well-informed decisions can help you improve the after-tax return of your investment in the long run.

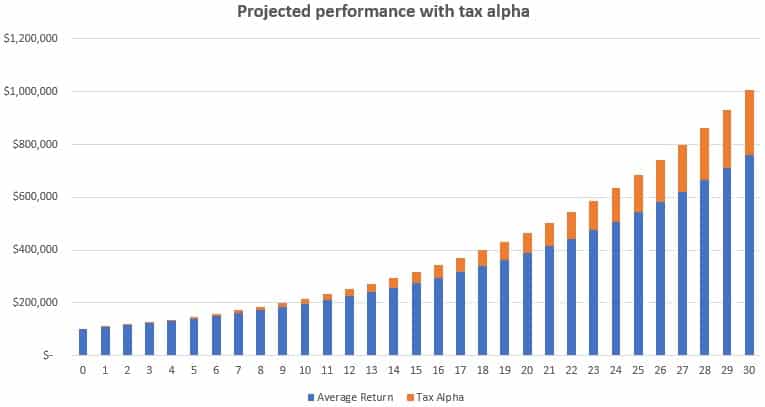

Assuming that you can generate 1% in excess annual after-tax returns over 30-year, your will investments can grow as much as 32% in total dollar amount.

1. Holistic Financial Planning

For our firm, achieving Tax Alpha is a process that starts on day 1. Making smart tax decisions is at the core of our service. Preparing you for your big day is not a race. It’s a marathon. It takes years of careful planning and patience. There will be uncertainty. Perhaps tax laws can change. Your circumstances may evolve. Whatever happens, It’s important to stay objective, disciplined, and proactive in preparing for different outcomes.

At our firm, we craft a comprehensive strategy that will maximize your financial outcome and lower your taxes in the long run. We start by taking a complete picture of your financial life and offer a road map to optimize your tax outcome. Achieving higher tax alpha only works in combination with your holistic financial plan. Whether you are planning for your retirement, owning a large number of stock options, or expecting a small windfall, planning your future taxes is quintessential for your financial success.

2. Tax Loss Harvesting

Tax-loss harvesting is an investment strategy that allows you to sell off assets that have declined in value to offset current or future gains from other sources. You can then replace this asset with a similar but identical investment to position yourself for future price recovery. Furthermore, you can use up to $3,000 of capital losses as a tax deduction to your ordinary income. Finally, you can carry forward any remaining losses for future tax years.

The real economic value of tax-loss harvesting lies in your ability to defer taxes into the future. You can think of tax-loss harvesting as an interest-free loan by the government, which you will pay off only after realizing capital gains. Therefore, the ability to generate long-term compounding returns on TLH strategy can appeal to disciplined long-term investors with low to moderate trading practices.

How does tax-loss harvesting work?

Example: An investor owns 1,000 shares of company ABC, which she bought at $50 in her taxable account. The total cost of the purchase was $50,000. During a market sell-off a few months later, the stock drops to $40, and the initial investment is now worth $40,000.

Now the investor has two options. She can keep the stock and hope that the price will rebound. Alternatively, she could sell the stock and realize a loss of $10,000. After the sale, she will have two options. She can either buy another stock with a similar risk profile or wait 30 days and repurchase ABC stock with the proceeds. By selling the shares of ABC, the investor will realize a capital loss of $10,000. Assuming she is paying 15% tax on capital gains, the tax benefit of the loss is equal to $1,500. Furthermore, she can use the loss to offset future gains in her investment portfolio or other sources.

3. Direct Indexing

Direct indexing is a type of index investing. It combines the concepts of passive investing and tax-loss harvesting. The strategy relies on the purchase of a custom investment portfolio that mirrors the composition of an index.

Similar to buying an index fund or an ETF, direct indexing requires purchasing a broad basket of individual stocks that closely track the underlying index. For example, if you want to create a portfolio that tracks S&P 500, you can buy all or a smaller number of 500 stocks inside the benchmark.

Owning a basket of individual securities offers you greater flexibility to customize your portfolio. First, you can benefit from tax-loss harvesting opportunities by replacing stocks that have declined in value with other companies in the same category. Second, you can remove undesirable stocks or sectors you otherwise can’t do when buying an index fund or an ETF. Third, direct indexing can allow you to diversify your existing portfolio and defer realizing capital gains, especially when you hold significant holdings with a low-cost basis.

4. Tax Location

Tax location is a strategy that places your diversified investment portfolio according to each investment’s risk and tax profile. In the US, we have a wide range of investment and retirement accounts with various tax treatments. Individual investment accounts are fully taxable for capital gains and dividends. Employer 401k, SEP IRA and Traditional IRA are tax-differed savings vehicles. Your contributions are tax-deductible while your savings grow tax-free. You only pay taxes on your actual retirement withdrawals. Finally, Roth IRA, Roth 401k, and 529 require pre-tax contributions, but all your future earnings are tax-exempt. Most of our clients will have at least two or more of these different instrument vehicles.

Now, enter stocks, bonds, commodities, REITs, cryptocurrencies, hedge funds, private investments, stock options, etc. Each investment type has a different tax profile and carries a unique level of risk.

At our firm, we create a customized asset allocation for every client, depending on their circumstances and goals. Considering the tax implications of each asset in each investment or retirement account, we carefully create our tax location strategy to take advantage of any opportunities to achieve tax alpha.

5. Smart tax investing

Smart tax investing is a personalized investment strategy that combines various portfolio management techniques such as tax-loss harvesting, asset allocation, asset location, diversification, dollar-cost averaging, passive vs. active investing, and rebalancing. The main focus of tax-mindful investing is achieving a higher after-tax return on your investment portfolio. Combined with your comprehensive financial planning, smart-tax investing can be a powerful tool to elevate your financial outcome.

Contact Us